Beyond the Headlines: Where Most Agency M&A Really Occurs

A 2025 recap of transaction volume, buyer demand, and the structural forces reshaping agency ownership as we move into 2026.

The independent insurance agency system continues to experience elevated M&A activity, but the story heading into 2026 is more nuanced than the headlines suggest. After more than a decade of heavy consolidation, the market is settling into what appears to be a “new normal;” one defined by sustained buyer demand, record-level valuations, and an ongoing wave of ownership transitions driven by planning – not panic.

Several long-term forces remain firmly in place. Agency principals are aging, with approximately 37% now over the age of 61. Valuations have climbed materially, increasing roughly 42% over the past eight years, and billion dollars of private capital, estimated at $85 billion invested or available for investment, continue to target the independent agency space. Layer on rapid technological change, increasing operational complexity, and AI-related uncertainty, and it’s clear why many agency owners are reassessing their long-term plans.

From an activity standpoint, M&A volume remains historically strong, even as it has cooled from peak levels. According to Optis Partners, 7,633 agency and broker transactions have occurred since 2016. When comparing five-year periods, transactions increased from 2,161 between 2013 and 2017 to 4,455 from 2021 through 2025. This is a 106% increase. While deal counts are down approximately 33% from the 2021 high, buyer interest remains robust, and well-run agencies continue to receive significant attention from multiple corners of the market.

Agency values ended 2025 at record levels. IA Valuations’ data shows the average EBITDA multiple across revenue categories at approximately 8.5x, with external sale revenue multiples averaging 3.0x. Values increased another 8.7% in 2025, supported by solid organic growth in a continuing hard market, the durability of recurring revenue with retention rates north of 90%, and strong operating performance, with average EBITDA margin around 27%. Fundamentals, not speculation, continue to underpin valuations.

One of the most misunderstood aspects of today’s M&A environment is where transactions are actually occurring. While Private Equity (PE) firms and publicly traded brokers dominate publicly reported deals, those transactions represent only a portion of total market activity. IA Valuations’ data indicates that 72% of ownership transactions in 2025 occurred between privately held retail agencies, including internal perpetuations and external sales to peer agencies. These transactions rarely make headlines, but they continue to drive the majority of ownership change in the IA system.

As we move into 2026, the independent agency landscape remains highly fragmented, with roughly 39,000 agencies still operating nationwide. Despite years of consolidation, opportunities for growth, succession, and transition remain plentiful. That said, the valuation environment is beginning to show signs of transition. While agency values remain historically strong, declining EV/EBITDA multiples among publicly traded insurance brokers are reshaping return expectations for institutional and strategic buyers alike. As those public benchmarks reset, valuation support is gradually shifting away from the headline premium multiples and back toward the durability and quality of underlying cash flow.

This dynamic places greater emphasis on confident profitability, commissions growth, and earnings resilience across all revenue groups. Put differently, valuation outcomes in the period ahead are likely to be driven less by how much of a premium buyers are willing to pay and more by how reliably agencies convert revenue into cash flow. The sections that follow – examining EBITDA margins, valuation multiples, and market benchmarks – explore these trends in detail to provide agency owners with clear, data-driven insight into how value is being created, and how it may be preserved, in a more disciplined M&A environment.

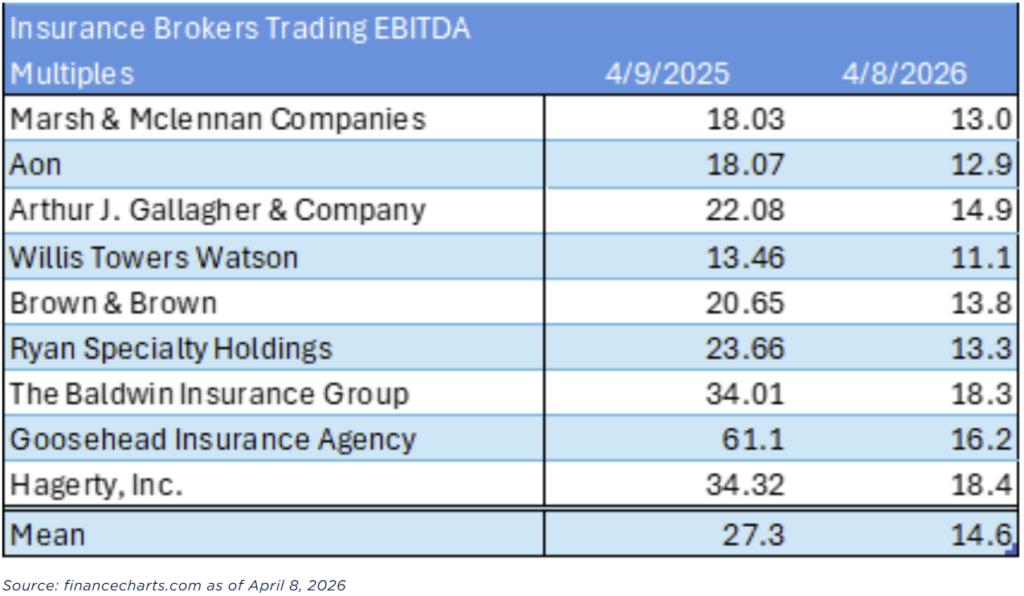

Public Broker Tracking

A Material Decrease in Value Over the Last Year

Over the last year, publicly traded insurance brokerages experienced a material contraction in EV/EBITDA trading multiples, with the average declining from 27.3x in April 2025 to 14.6x in April 2026. This pullback reflects broader market pressures, including higher interest rates, increased cost of capital, and heightened investor scrutiny of long-term growth assumptions.

While privately held insurance agencies will never trade at public company multiples, these public valuations set the ceiling for the entire valuation ecosystem. As that ceiling compresses, pressure inevitably works its way down through the entire insurance agency landscape.

Ultimately, while agency values remain historically strong, the market is transitioning from a multiple-driven valuation back to a cash-flow-driven valuation. Agencies that demonstrate consistent, defendable pro forma profitability will remain best positioned, regardless of size, as capital becomes more disciplined across the buyer landscape.

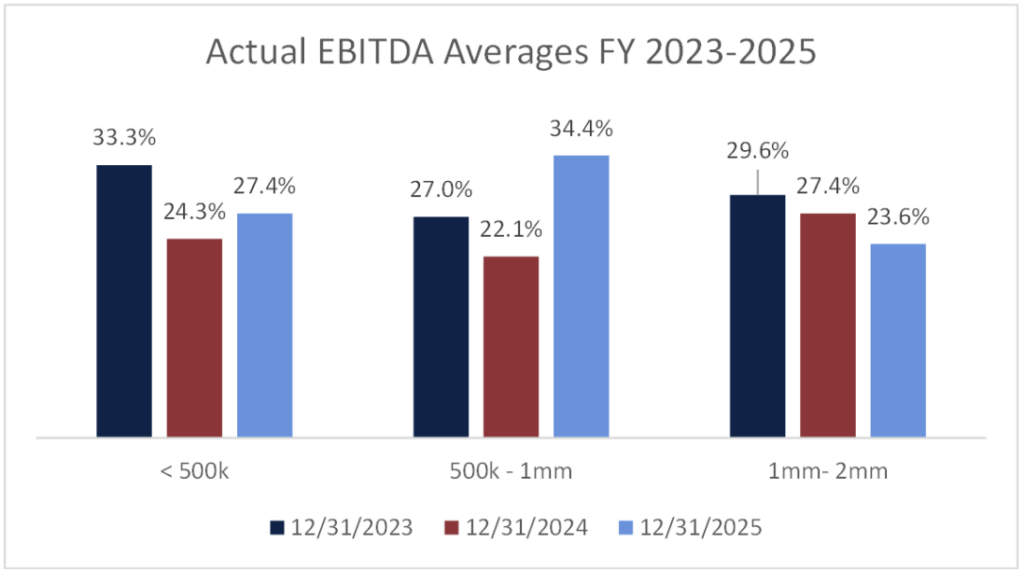

Agency Actual Profitability 2023 – 2025

Profit Sharing Boosts the $500k – $1M Revenue Group

Agencies with Less Than $500K Revenue

Actual EBITDA margins for agencies under $500k were far more volatile than their pro forma counterparts. Average actual margins declined sharply from approximately 33.3% in 2023 to 24.3% in 2024, before rebounding to 27.4% in 2025. This volatility reflects the sensitivity smaller agencies have to variability in producer compensation, contingencies, and discretionary owner expenses.

The partial rebound in 2025 is encouraging but reinforces why buyers heavily rely on pro forma analysis when valuing agencies of this size. Actual performance alone can materially understate future earnings power in any given year.

Agencies with $500K – $1M in Revenue

The $500k – $1M group experienced the widest range of actual EBITDA outcomes over the last three years. Margins dipped from 27.0% in 2023 to 22.1% in 2024, before surging to 34.4% in 2025.

This sharp rebound suggests 2025 was an exceptionally strong year operationally, driven largely by profit sharing returning and expense efficiency.

However, the magnitude of the swing also highlights the inherent earnings variability in this group. While actual results can outperform expectations in strong years, they remain less predictable than pro forma margins, which continue to anchor valuation analysis.

Agencies with $1M – $2M in Revenue

Actual EBITDA margins for $1M – $2M agencies displayed a gradual downward trend across the period. Average margins declined from 29.6% in 2023 to 27.4% in 2024, and further to 23.6% in 2025.

Despite this decline in reported results, pro forma margins moved in the opposite direction, signaling that the margin shrinkage is largely attributable to a softening market rather than structural weakness.

in this revenue group, agencies reinvest more aggressively in staff and technology, temporarily lowering actual profitability.

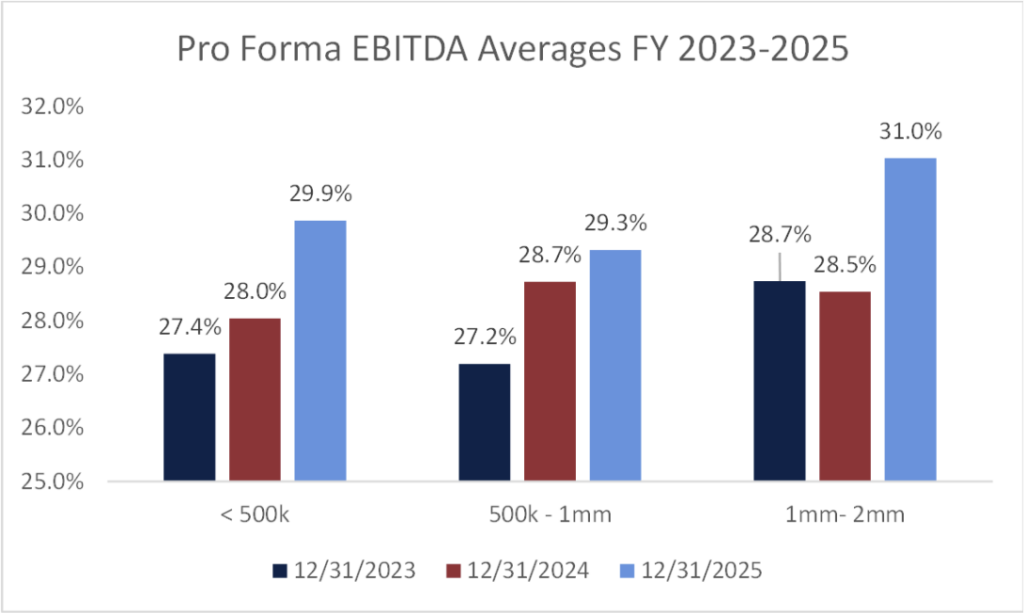

Pro Forma Profitability 2023 – 2025

Profitability after removing non-recurring or tax strategy expenses

Agencies with Less Than $500K in Revenue

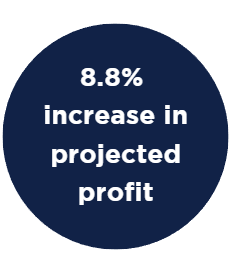

Over the last three valuation years, agencies with less than $500k in annual revenue have demonstrated a steady and encouraging upward trend in pro forma EBITDA margins.

Average pro forma profitability increased from approximately 27.4% in 2023 to 28.0% in 2024, before rising again to nearly 29.9% in 2025.

This trend suggests that even the smallest agencies are becoming more disciplined in normalizing expenses and removing owner-specific inefficiencies when presenting forward-looking profitability.

Agencies with $500K – $1M in Revenue

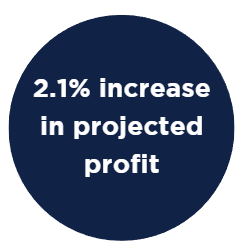

The $500k – $1M group continues to exhibit consistent margin expansion in pro forma EBITDA, reinforcing the advantages of scale that begin to emerge at this size. Pro forma EBITDA margins rose from roughly 27.2% in 2023 to 28.7% in 2024, followed by a modest increase to 29.3% in 2025.

This group begins to benefit from economies of scale, being able to generate more revenue with the similar if not same amount of expense. The steady upward trend reflects growing confidence from buyers and lenders that these agencies can sustain higher normalized profitability over time, even as the market environment softens.

Agencies with $1M – $2M in Revenue

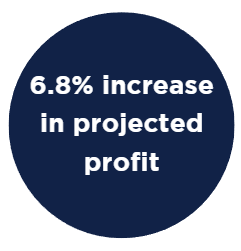

Agencies in the $1M – $2M revenue range posted the strongest pro forma profitability gains among the analyzed tiers. After holding relatively flat from 28.7% in 2023 to 28.5% in 2024, average pro forma EBITDA margins jumped materially to approximately 31.0% in 2025.

This revenue group increase underscores the meaningful economies of scale agencies often unlock once they surpass $1M in revenue. More diversified books, deeper staffing infrastructure, and better carrier arrangements allow for confidence in forward-looking margins. For buyers, this revenue group increasingly represents a “sweet spot” where operational scale meets strong pro forma profitability.

When Values Drive Value

A Thoughtful Agency Transition Done Right

Growing up the son of an independent agent, Alan Sills of Ralph P. Sills Insurance Agency, didn’t originally plan to be part of the family business. He pursued a legal career, attending law school and practicing as an attorney for several years before his father asked him for help with the agency. That request ultimately led him back to insurance, where he has remained ever since.

As a small mom-and-pop agency, they built a niche serving other small businesses and developed a very loyal client base in the Cleveland suburbs. That loyalty extended beyond clients; the agency was supported by a long-tenured and committed staff. “We grew up together and stayed together,” said Alan. As he approached retirement and started planning, Alan knew an external sale would be necessary. His daughters were not in the industry and were not looking to enter it, and many of his long-standing employees were planning to retire on a similar timeline.

Alan hoped to sell the agency to a friendly competitor or local firm. He always kept his ears open for third parties who seemed interested in selling or purchasing his agency. He often got letters from agents who were interested in purchasing his agency, and instead of disregarding these, he put them in a file to refer back to later. He also relied on OIA and began to consider IA Valuations’ Agency Link service as a resource.

Achieving a fair and equitable financial outcome was important, as it is for all business transactions, though it was not his only objective. “Now, this is where I’ll sound really altruistic,” Sills said, referring to the other primary focus of his transition: finding a buyer to maintain the agency’s culture and customer service standards. As is the case for many independent agents, Alan viewed his clients and community as the foundation of his business. Ensuring that any successor would serve clients with the same care and commitment was essential to him.

While his plan had been formulating for a while, he didn’t put pen to paper on his transition until a couple of years ago. While working closely with an attorney, a close friend and long-term business partner, he decided to reach out to the IA Valuations team for assistance in selling his agency. The process began in late 2024, and by spring of 2025, a Letter of Intent was signed with the Evarts Tremaine Agency – a local Cleveland agency whose culture aligned well with Alan’s values and with whom he felt confident entrusting his clients.

Following months of due diligence and contract negotiations handled by each party’s legal teams, the sale of Ralph. P Sills Insurance Agency was finalized in August 2025. Alan remained closely involved during the early stages, providing client files, operational insights, and guidance on agency systems. This has gradually scaled back over time, and he now works part time. His primary focus is on easing the transition for his loyal clients and helping them get used to the new normal with the Evarts Tremaine team.

In August of this year, Alan’s one-year contract with the new owners will conclude, though his duty doesn’t end there. He remains willing to assist as needed, and the Evarts Tremaine team continues to value his experience and insight. Reflecting on the transition, Alan expressed confidence in the outcome, noting that his clients remain well cared for. “He’s the kindest and most professional gentleman,” Sills said of agency principal John Hannon.

Alan credits much of the smooth transition to the support provided by IA Valuations. He truly believes that the guidance of Jeff Smith and Jarod Steed played a significant role in helping him reach this point. Knowing he had a knowledgeable third-party team to rely on to bring buyers to the table, negotiate deals, review contracts, and answer his questions, provided the peace of mind that he needed so he could focus on the most important pieces of the transition, rather than get caught up in the minutia.

When asked about his post-retirement plans, Alan chuckled. “I don’t know how I’m going to spend my time. I want to enjoy what’s left in life with my wife – whatever God brings to us.” Staying active, traveling, and spending time with his daughters and grandchildren are all parts of his plan. He has worked hard for decades, much of this time spent working alongside his wife, Michelle. This will bring a new dynamic for the Sills family, one which they are excited to embark upon.

About IA Valuations and Agency Link – Founded in 2017, the IA Valuations team has performed over 400 valuations to independent insurance agencies across the U.S. Our advisors have 30+ years of experience guiding agency owners on maximizing their agency value, planning, and legal needs for ownership transition. In addition, IA Valuations has provided perpetuation planning, financial modeling and business planning for independent insurance agencies. Finally, IA Valuations has advised dozens of agency owners on selling their agencies through our Agency Link process. Agency Link is a platform that connects buyers and sellers together to further the growth and strength of the IA system. To learn more about IA Valuations, please visit IAValuations.com or contact@iavaluations.com.

The information provided in these documents is general in nature and shall not be construed as personal legal, tax or financial advice for your situation. Please contact@iavaluations.com to discuss your personal situation.

Copyright ©2026 by IA Valuations and Ohio Insurance Agents Association (OIA). All rights reserved. No portion of this document may be reproduced in any manner without the prior written consent of IA Valuations or OIA. In addition, this document may not be posted as a link on any public or private website without the prior written consent of IA Valuations or OIA.

At OIA and IA Valuations, we use AI tools (including, but not limited to, Co-Pilot, ChatGPT, Grammarly, and design platforms with AI features) to support the development of communications, professional development resources, and marketing materials. AI assists with drafting, analysis, and design but never fully automates these processes.

All AI-supported content is reviewed and approved by OIA/IA Valuations staff to ensure accuracy, relevance, and alignment with the independent insurance industry. We are committed to transparency, data protection, and ethical use of AI as a supportive tool—not as a replacement for human expertise.