There are many ways to increase agency value, but there are always questions. Is organic or acquired growth better? What do I need to think about when considering an acquisition? How do I create the financial model to decide what to offer in an acquisition? What is the benefit of a new producer? Is an unsuccessful producer a waste of my resources? The burning question is always, is there a “best” way?

In this 3-part business case series, we will attempt to answer these questions and more. We will do so by analyzing the cash flow and agency value impacts for a control agency in 3 different scenarios:

- A revenue acquisition

- A talent acquisition

- Growing organically

The insurance market is starting to soften, and that means the eye-popping revenue growth numbers for agencies from the hard market will start to settle down. Agencies looking for sustained growth will have to implement other methods to maintain the growth they experienced during the hard market. In this edition of our Business Case series, we are going to analyze a growth through “revenue acquisition.” A revenue acquisition is one where the acquiring agency is purchasing a book of business without an expectation that the owner/operator will remain with the acquirer and produce in a meaningful way. Put in other terms, the acquirer’s primary benefits are the revenue of the book being acquired, strengthening the acquirer’s position with their key carriers, and keeping the competition away, but it is not a talent acquisition.

The Case Study

Imagine two agencies:

- The acquirer, a $1 million revenue agency with a 25% EBITDA margin and an 8.25x EBITDA multiple applied as their control valuation.

- The acquirer is a strong independent agency – exceptional customer service, a steady stream of referral business, and a team including two validated producers

- The seller, a $250,000 revenue agency, single owner/producer nearing retirement with one service employee also planning to stay on after the acquisition.

- The seller represents many agencies in today’s market: a “Main Street” shop, predominantly personal lines, built over time but now facing a succession dilemma.

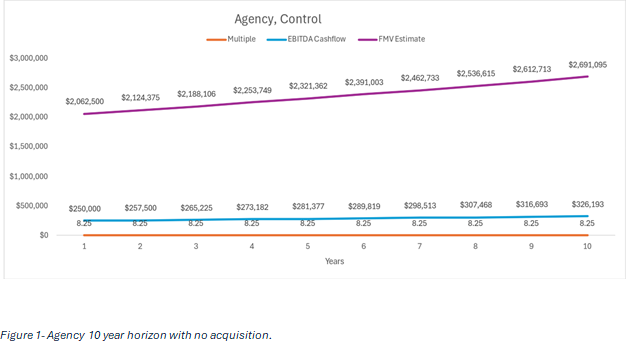

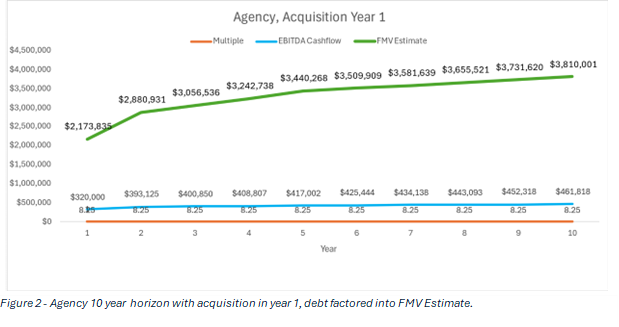

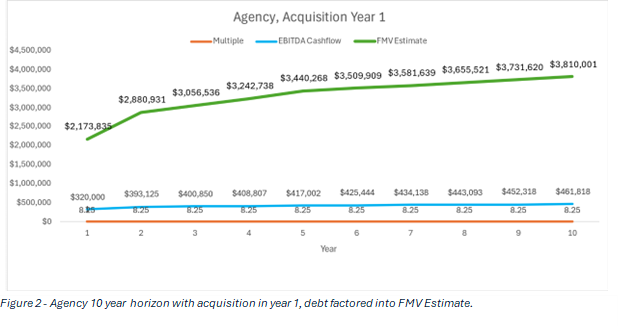

This case study will look at two scenarios over the course of 10 years.

- The control scenario – the acquirer continues organic growth at 3% annually.

- Acquisition scenario – the acquirer buys the $250,000 agency in year one while growing their original book at the same 3%.

For our case study, our “Fair Market Value (FMV) Estimate” is this simple equation:

Case Study Value Estimate = EBITDA cashflow * multiple of EBITDA – liabilities

Key Variables to an Acquisition

Retention of Personal vs. Commercial vs. Employee Benefit books – This is the most important factor in an acquisition. The risk of not retaining a meaningful percentage of revenue after an acquisition is lower with a mostly personal lines book due to their higher policy count and lower premium volume per account nature; however, they are not as valuable externally. Meanwhile, commercial and EB books are currently more valuable externally but could be higher risk for switching agents during an ownership transition and require a greater level of account management to retain post-acquisition due to their added complexities. Our scenario: the seller is 80-90% personal lines. While the seller is still with the agency, 90% of the revenue is retained and after the seller retires or leaves 85% of the original revenue is retained going forward.

Key carrier overlap – Look for this in an acquisition like the one described. Be sure to review the following in the due diligence process: 5-year loss ratio, premium growth, and average age of the clients. You want to make sure you are acquiring a book that has a long runway on the lifetime value of client equation. Our scenario: the seller’s key carriers align with the acquirer.

Purchase price – Much of what will determine whether this will be a good or bad investment is the purchase price. Be fair, but do not overpay in this scenario. There is not a lot of strategic value in this acquisition, so there is no reason to overpay for the agency. In our results selection throughout this series, you can compare our 10-year return on investment calculations for each scenario. Our scenario: the acquirer is paying 2.25x for the seller’s book.

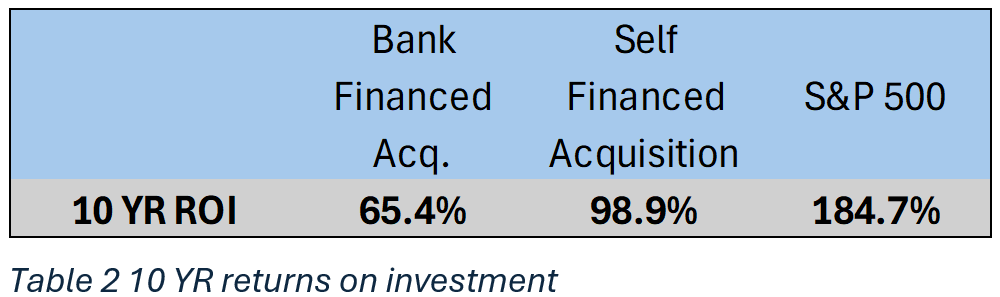

Financing – Along with purchase price, the financing option used for the acquisition can really impact the value gained from a transaction. See Table 2 below to compare a self-financed ROI to a bank-financed one.

Synergy – Synergy refers to how efficiently the acquirer can assimilate the new book and talent into its existing operations. An acquirer should measure or estimate how much additional operating expense they expect to spend on an ongoing basis for the new book. A way to estimate this could be looking at your current operating expense to revenue ratio and project forward. If an acquirer is able to assimilate a new book of business and retain it for even less cost, 12, 10, or even 5% of the net revenue gained from the acquisition, then that means more cashflow for them. Our scenario: we used 15% operating cost/revenue.

Pro Tip – The best way to acquire an agency in this scenario is with a two-part offer: down payment for 50% of the agency at closing, and then a 2-year holdback to be paid in years 1 and 2 based on the percentage of revenue retained.

Results: How long to make my money back?

The figure above is only considering cashflow from the acquired book of business. The orange bar represents the year when the acquisition starts making money for the acquirer. The terms of the loan are below:

Results: Is this a good investment?

These ROI results were based on the value gained in the acquisition scenario versus the control scenario. These numbers, when compared to an investment in the S&P 500, are not compelling; however, to get a 187.4% return assumes you have $3M to invest over a 10-year period, which is not a common scenario for most independent insurance agency owners. For an insurance agency owner to get a safe 65%, 10-year ROI is a fairly solid return in a business that you know intimately and significantly enhances your annual cashflow and value of your agency.

The Takeaway: Acquisition as a Strategic Growth Engine

This case study underscores a critical point: growth by acquisition can be an incredibly effective strategy to grow value and profits over time if you have a good acquisition and integration strategy.

There is value generated for an agency owner when they perform a revenue acquisition; however, the argument is not as compelling as the future cases we will look at with a strategic acquisition. Revenue acquisitions increase the baseline value of the agency, in this case by $1.1M over 10 years and adds $130K to annual profits, but it is not going to create generational wealth opportunities like strategic acquisition may provide.

In real life, these acquisitions may look like an emergency purchase of a friendly competitor or an owner selling with a 0-1 year retirement timeline. These situations are necessary for the industry, but they are not the best long-term value creation strategies for buyers or sellers.

For agencies considering growth through acquisition, this case study highlights key factors to consider:

- Retention risk: Will the acquired clients stay? Do you have an integration plan that ensures a smooth transition of clients, carriers, and staff?

- Talent pipeline: Can you integrate and retain key people?

- Financial readiness: Do you have a strategy for the financial component of the acquisition? Do you have trusted advisors to work with?

- Operational fit: Do your markets, business mix, type of clients, and service philosophies align?

Ultimately, a revenue acquisition is more like a one-time transaction, whereas in an ideal world, an acquisition is not just a transaction; it’s a transformational event. When done thoughtfully, it can compress years of organic growth into a few short years and dramatically increase an agency’s value. This requires preparation, integration, and focus on the long game. In our next case study, we will look at the tangible impact of a strategic agency acquisition.

If you have questions about this case study or what IA Valuations to look at specific aspects of your agency, please contact Jarod Steed at jarod@iavaluations.com to get started.

By: Jarod Steed, Business Planning & Valuations Analyst

Jarod Steed is the Business Planning & Valuation Analyst for the IA Valuations team. A graduate of The Ohio State University, he holds a bachelor’s degree in business administration with a specialization in finance and a minor in economics. Jarod’s professional background includes accounting and operations analysis in the Insurtech industry. He has a passion for delivering insightful numbers and thoughtful analysis. Jarod enjoys working closely with independent insurance agents in the valuation, consulting, and M&A space and helping them understand their agency better.

About IA Valuations and Agency Link – Founded in 2017, the IA Valuations team has performed over 270 valuations to independent insurance agencies across the U.S. Our advisors have 25+ years of experience guiding agency owners on maximizing their agency value, planning, and legal needs for ownership transition. In addition, IA Valuations has provided perpetuation planning, financial modeling and business planning for independent insurance agencies. Finally, IA Valuations has advised dozens of agency owners on selling their agencies through our Agency Link process. Agency Link is a platform that connects buyers and sellers together to further the growth and strength of the IA system. To learn more about IA Valuations, please visit IAValuations.com or contact@iavaluations.com.

The information provided in these documents is general in nature and shall not be construed as personal legal, tax or financial advice for your situation. Please contact@iavaluations.com to discuss your personal situation.

Copyright ©2025 by IA Valuations and Ohio Insurance Agents Association (OIA). All rights reserved. No portion of this document may be reproduced in any manner without the prior written consent of IA Valuations or OIA. In addition, this document may not be posted as a link on any public or private website without the prior written consent of IA Valuations or OIA.