Taxation Implications of Different Corporate Structures

As another tax season approaches, now is an ideal time for independent insurance agency owners to reassess their corporate structure and evaluate whether they are positioned to minimize their annual tax burden – while also preparing for the long-term tax implications of a future sale. A thoughtful tax review with your professional advisors can help you understand both your immediate obligations and the strategic opportunities available to you.

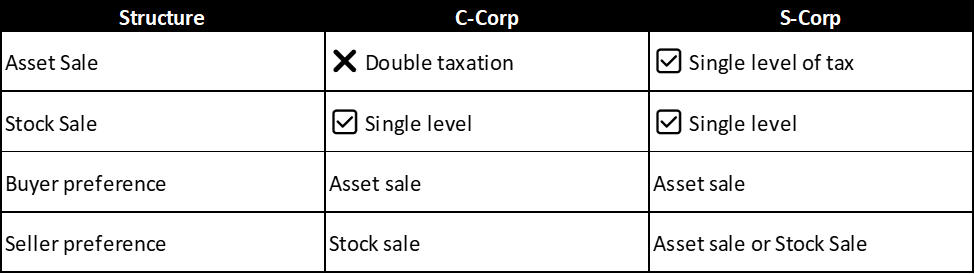

How Corporate Structure Affects a Future Sale

Whether your agency is acquired through a stock sale or an asset sale has major tax and liability implications, and your current entity type often determines the likely path forward.

Asset Sales

In an asset sale, the buyer generally acquires the agency’s intangible and tangible assets but avoids inheriting existing liabilities. Buyers strongly prefer this structure because it reduces risk and often provides tax advantages.

Agencies structured as S-Corps or LLCs also avoid double taxation on the proceeds of an asset sale because income passes directly to the owners and is taxed at their individual rates.

Stock Sales

Sellers tend to favor stock sales. Proceeds receive capital gains treatment, and the tax rate is determined by how long the stock was held. However, a buyer inherits all liabilities – known and unknown – making stock purchases riskier and less appealing to acquirers.

The C-Corp Challenge

For C-corporations, asset sales are less tax-efficient because sale proceeds are taxed twice: first at the corporate level and again when proceeds are distributed to shareholders. This makes early planning essential if a C-Corp is considering a future sale.

Big Picture Summary

To illustrate why corporate structure matters, particularly in an external transaction, I have included a summary chart of the advantages and disadvantages for each type of structure in a deal.

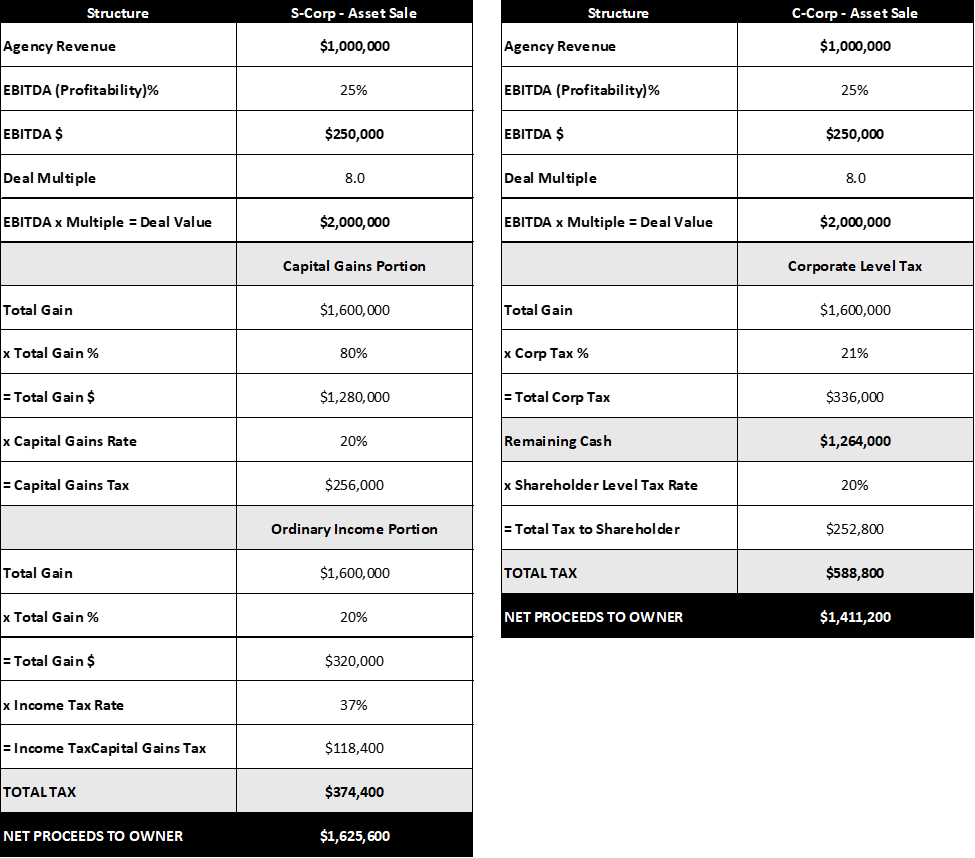

S-Corp Asset Sale vs. C-Corp Asset Sale

In an S-Corp asset sale, buyers purchase the agency’s assets (typically, the bulk of the value is the renewal list/expirations). When the agency sells the assets, the gains flow through to shareholders. Then, the shareholders pay capital gains tax, but no corporate-level tax.

Compare this to a C-Corp asset sale. In this scenario, the corporation pays 21% federal corporate tax on gains. Then, the shareholders pay individual taxes on proceeds that are distributed as dividends or liquidation, based on their own particular tax brackets.

It is clear that in most cases, S-Corps are far more tax-efficient for sellers, especially if the buyer insists on an asset sale. Buyers usually prefer asset deals for many reasons, including a step-up in basis, future depreciation, and avoiding unknown liabilities tied to the corporation. Therefore, C-Corp sellers are often pressured into asset deals and higher taxes, whereas S-Corp sellers can accept asset deals with minimal penalty.

So, what does this mean in the real world? The following example will compare the sale of two $1 million insurance agencies – one an S-Corp, and one a C-Corp – and the tax implications for each.

Agency Sale Scenario

To compare the tax impacts under each scenario, I used the following assumptions:

- Sale Price = $2,000,000

- Seller Basis in business = $400,000

- Total Gain = $1,600,000

- 80% Capital Gain

- 20% Ordinary Income

- Federal Rates:

- Capital Gains: 20%

- Ordinary Income: 37%

- Corporate Tax (C-Corp): 21%

In this comparison, it is quite clear that the S-Corp was the preferable arrangement for tax purposes. The S-Corp seller took home an additional $214,400 in the sale. The net proceeds to the C-Corp were only 86.8% of the total received by the S-Corp.

What Our Data Shows

Although the number of agencies registered as C-Corps has decreased over the years, we examined the data in the IA Valuations database to get more insight into the market. Across several hundred agency valuations conducted between 2023 and 2025, approximately 15.6% of agencies were still organized as C-corporations, with an average owner age of 62.6, and over 54% of these owners were past age 65.

These insights highlight an important trend: many owners at or past retirement age remain in a structure that is often less advantageous in a sale, particularly when compared to S-Corps and LLCs. Industry benchmark studies confirm a substantial difference between the prevalence of C-Corp and more tax-efficient structures.

If you are planning to retire or transition ownership within the next several years, shifting to a different entity type sooner rather than later can help ensure future tax benefits, especially given the multi-year waiting period required for certain conversions.

Planning Strategies: What Agency Owners Should Do Now

Each agency’s situation is unique – but certain actions will benefit nearly every owner:

- Meet with Your Tax Advisor. Ask them to walk you through multiple sale and ownership-transition scenarios. This will help you understand both your annual tax obligations and long-term implications.

- Review Whether Your Current Entity Type Still Fits. Your structure affects your tax rate, QBI eligibility, and how a sale will be taxed. It may be advantageous to consider reorganizing sooner rather than later.

- Prepare for Possible Tax Law Changes. The passage of the legislation known as the “One Big Beautiful Bill Act” in July of 2025 made permanent many of the key provisions of the 2017 Tax Cuts and Jobs Act, which were set to expire at the end of 2025. This eliminated the possibility of potential changes to capital gains rates.

- Conduct Long-Term Scenario Planning. Your accountant, attorney, and valuation consultant can model multiple outcomes to help you identify the structure that best aligns with your retirement timeline and agency goals.

A comprehensive tax review is no longer optional; it’s a strategic necessity. Whether you plan to keep growing your agency, transition ownership, or explore a future sale, your corporate structure directly influences your tax burden, your valuation, and the net proceeds you will ultimately retain.

By taking time now to review your structure, understand potential legislative changes, and work closely with your professional advisors, you can position your agency – and yourself – for a stronger future. For advice on how to get started, reach out to Craig Niess, Director of Business Planning & Valuations at IA Valuations, at craig@iavaluations.com or at (216) 288-8409.

By: Craig Niess, CVA, MBA

About IA Valuations and Agency Link – Founded in 2017, the IA Valuations team has performed over 400 valuations to independent insurance agencies across the U.S. Our advisors have 30+ years of experience guiding agency owners on maximizing their agency value, planning, and legal needs for ownership transition. In addition, IA Valuations has provided perpetuation planning, financial modeling and business planning for independent insurance agencies. Finally, IA Valuations has advised dozens of agency owners on selling their agencies through our Agency Link process. Agency Link is a platform that connects buyers and sellers together to further the growth and strength of the IA system. To learn more about IA Valuations, please visit IAValuations.com or contact@iavaluations.com.

The information provided in these documents is general in nature and shall not be construed as personal legal, tax or financial advice for your situation. Please contact@iavaluations.com to discuss your personal situation.

Copyright ©2026 by IA Valuations and Ohio Insurance Agents Association (OIA). All rights reserved. No portion of this document may be reproduced in any manner without the prior written consent of IA Valuations or OIA. In addition, this document may not be posted as a link on any public or private website without the prior written consent of IA Valuations or OIA.

At OIA and IA Valuations, we use AI tools (including, but not limited to, Co-Pilot, ChatGPT, Grammarly, and design platforms with AI features) to support the development of communications, professional development resources, and marketing materials. AI assists with drafting, analysis, and design but never fully automates these processes.

All AI-supported content is reviewed and approved by OIA/IA Valuations staff to ensure accuracy, relevance, and alignment with the independent insurance industry. We are committed to transparency, data protection, and ethical use of AI as a supportive tool—not as a replacement for human expertise.